AI is transforming financial services and fintech by improving efficiency, cutting costs, and driving revenue growth. Here's what you need to know:

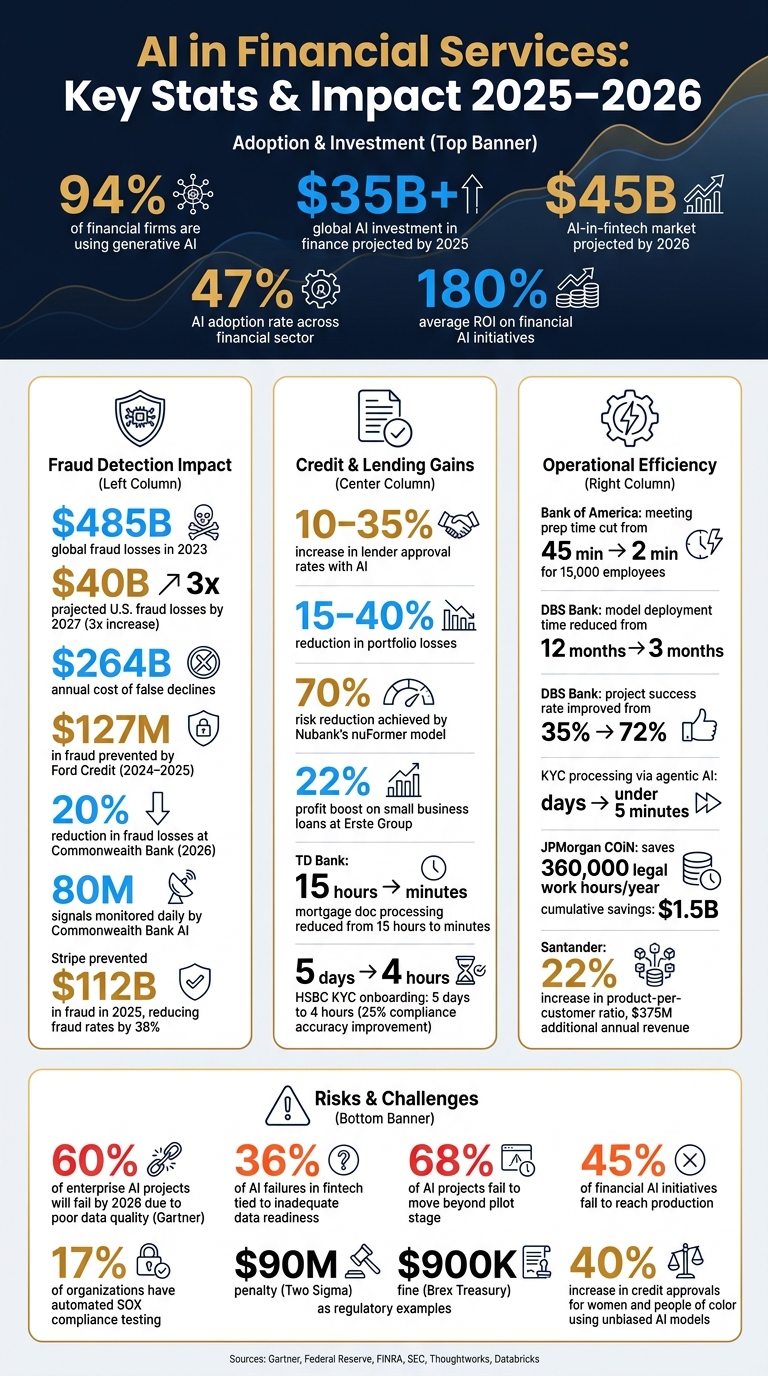

Adoption: 94% of financial firms are using generative AI, with global AI investments in finance projected to exceed $35 billion by 2025.

Key Impacts: AI has reduced operating costs by up to 20% and increased revenues for 64% of firms. Applications include fraud detection, credit decisioning, and personalized customer services.

Technologies: Tools like machine learning, deep learning, generative AI, and agentic AI are reshaping processes like risk management, compliance, and customer interactions.

Use Cases: AI helps detect fraud in real-time, automate credit scoring with detailed financial insights, and deliver tailored financial advice via virtual assistants.

Challenges: Successful AI adoption depends on robust data infrastructure, regulatory compliance, and managing risks like bias, explainability, and cybersecurity.

AI is no longer experimental - it's a core part of financial operations, with the potential to redefine how financial institutions operate. For businesses, the focus now shifts to scaling AI responsibly while meeting evolving regulatory standards.

AI in Financial Services: Key Stats & Impact 2025–2026

AI for Financial Services

sbb-itb-18d4e20

Key AI Use Cases in Financial Services

AI is transforming financial services by addressing specific challenges with measurable results. Three areas where its impact is particularly clear are fraud detection, credit decisioning, and personalized customer experiences. These use cases highlight how AI improves efficiency, reduces risk, and enhances customer interactions.

Fraud Detection and Security

Fraud is an escalating issue. In 2023, global financial losses from fraud surpassed $485 billion. By 2027, generative AI could drive U.S. fraud losses to $40 billion, a threefold increase from 2023. False declines - when legitimate transactions are wrongly flagged - add another layer of complexity, costing the industry $264 billion annually, nearly five times the direct fraud losses. The challenge is not just catching fraud but doing it without alienating legitimate customers.

Graph Neural Networks (GNNs) have become a game-changer. By mapping relationships between users, devices, and IP addresses, they can uncover fraud rings that traditional models miss.

"Fraudsters have evolved from isolated actors into sophisticated, coordinated networks. They hide in the relationships that traditional models were built to ignore." - Thoughtworks

Real-world examples drive home the point. Ford Credit deployed a real-time fraud detection system using knowledge graph technology and Google Cloud's Vertex AI Pipelines, preventing over $127 million in fraudulent purchases between 2024 and early 2025 - all without adding delays for customers. Similarly, Commonwealth Bank introduced an agentic AI system in April 2026 that monitors 80 million signals daily, leading to a 20% reduction in fraud losses in the first half of 2026 compared to the prior year.

"The technology allows us to identify unusual events in highly complex patterns of activity at far greater speed and scale, helping us detect emerging threats sooner and update our controls faster." - James Roberts, Executive General Manager of Fraud and Scams, Commonwealth Bank

Beyond fraud prevention, AI is also reshaping how credit decisions are made.

Credit Scoring and Automated Underwriting

Traditional credit scoring methods rely on outdated data, often missing the nuances of a borrower’s financial situation. AI changes the game by incorporating real-time transaction-level data - including cash flows, spending habits, and seasonal revenue trends - to paint a more accurate picture of financial health. This approach has been shown to increase lender approval rates by 10% to 35% without raising risk and to reduce portfolio losses by 15% to 40%.

The operational improvements are equally impressive. TD Bank Group implemented an AI-powered system in January 2026 to process mortgage documents. Tasks like extracting income data from pay stubs and verifying IDs, which previously took 15 hours, now take just minutes.

"The mortgage loan process also has measurable friction, one where a human still needs to be accountable for the final decision. That's almost a perfect use case... you've shortened the time for the credit decision." - Brad Leimer, Founder, Leimer One Advisors

Other institutions are seeing similar results. Nubank introduced "nuFormer", a transformer-based risk model, in May 2026, achieving a 70% reduction in risk for comparable borrower groups. This helped them secure their largest credit card market share gain in Brazil in a decade while keeping write-offs steady at 2.8% to 2.9%. At Erste Group, AI-driven individualized loan pricing replaced manual branch-level processes, boosting profits on small business loans by 22%.

While AI streamlines credit evaluations, it also plays a key role in enhancing customer engagement.

Personalized Financial Services

More than 50% of U.S. adults have used generative AI for financial advice, and 62% of consumers trust their primary bank to deliver these services more than they trust big tech companies. This trust presents a major opportunity for financial institutions.

AI is driving two major shifts in personalized services. First, it’s empowering human advisors by automating tedious prep work. Bank of America integrated AI tools with Salesforce and Zoom in March 2026, enabling 15,000 employees across its Merrill Lynch and Private Bank units to cut meeting prep time from 45 minutes to just 2 minutes. Second, AI is creating entirely new client-facing experiences. For example, Citi Wealth launched "Citi Sky" in April 2026, an AI-powered virtual wealth assistant built on Google Cloud and Google DeepMind. Using real-time avatar technology and live audio/video models, it provides Citigold clients with instant market insights and proactive guidance on events like CD maturity.

"With Citi Sky, you simply ask – and act. This is the shift from interface to intelligence, from transactions to outcomes." - Andy Sieg, Head of Wealth, Citigroup

AI proves most effective when embedded into specific workflows that face significant challenges. Financial institutions achieving the best results are those that pinpoint bottlenecks and design AI solutions to address them.

Building AI-Ready Financial Products

Creating AI-driven solutions for financial services isn't just about leveraging advanced models; it requires strong engineering foundations and careful governance. Success hinges on prioritizing data infrastructure, system design, and model operations from the outset.

Data Infrastructure and Governance

One of the biggest hurdles in financial AI projects is poor data quality. According to Gartner, 60% of enterprise AI projects will fail by 2026 due to a lack of AI-ready data. Similarly, 36% of AI failures in fintech are tied to inadequate data readiness.

A practical way to address this is by using a Medallion Architecture. In this setup:

Bronze layer: Where raw data is stored.

Silver layer: Data is standardized and validated.

Gold layer: Only certified data, with clear ownership, is used for modeling.

This structure ensures a transparent and auditable data trail, which is crucial for regulatory compliance. For instance, SOX Section 404 mandates detailed documentation of every data transformation, including source information, transformation logic, destination details, governing controls, and timestamps. Yet, only 17% of organizations have automated SOX compliance testing. Automating these processes through declarative pipelines can make audits smoother and less costly.

"Evidence must be produced as a byproduct of how models are built, not reconstructed after the fact. That is a platform problem, not a policy problem." - Databricks

Another key decision is to manage both traditional machine learning models and generative AI systems under a single governed framework. This unified approach prevents fragmented audit trails and avoids duplicating compliance efforts.

System Architecture for AI

Once a solid data foundation is in place, the next step is designing a system architecture that balances speed and compliance.

Production-grade financial AI systems often use layered architectures with strict latency targets. Here’s a typical five-layer setup used in high-throughput applications like fraud detection:

Layer

Component

Latency Budget

1. Ingestion

Kafka / Kinesis

≤10ms

2. Feature Store

Redis / DynamoDB

≤15ms

3. Scoring

XGBoost / LightGBM

≤20ms

4. Orchestration

Decision Logic

≤15ms

5. Compliance

Audit Logging

≤5ms

The Feature Store layer is especially critical. Without it, discrepancies can arise between the features used during training and those available during real-time inference - a problem known as training–serving skew. A dedicated feature store ensures consistent, low-latency access to both historical and real-time data.

For more complex workflows like KYC (Know Your Customer) or AML (Anti-Money Laundering), an agentic orchestration model is proving effective. This involves a Supervisor Agent coordinating specialized sub-agents - such as those for Identity, Fraud, and Compliance - operating in parallel. This approach has reduced KYC processing times from days to under five minutes. For simpler use cases, an API-based wrapper can enable fast prototyping with latency tolerances of 1–5 seconds.

AI Model Lifecycle and Scalability

Deploying a model is just the beginning. Financial AI systems require ongoing management throughout their lifecycle, from data sourcing and feature engineering to validation, deployment, monitoring, and eventual retirement. Documentation at every stage is essential.

Monitoring model performance is vital. For example, the Population Stability Index (PSI) is a useful metric for detecting model drift. If PSI exceeds 0.2, a review is needed, and values above 0.25 signal the need for retraining. Without these safeguards, performance issues might go unnoticed until they cause significant problems.

Consider HSBC’s AML implementation: by replacing their outdated system with a custom AI solution and maintaining active monitoring, they identified 2–4 times more suspicious activities while cutting false positives by 60%. Achieving this level of performance requires tools like versioned features, champion/challenger testing, and dynamic model cards that automatically update with each production version.

For high-risk applications such as credit scoring, fraud detection, and underwriting, human oversight is essential. Frameworks like SMCR and the revised April 2026 interagency MRM guidance require human-in-the-loop checkpoints for banking organizations with over $30 billion in total assets. Tiering models by their impact ensures that high-stakes decisions (Tier-1) receive rigorous oversight, while lower-stakes systems maintain efficiency.

Managing Risk and Compliance in AI Adoption

Bringing AI into finance requires more than just technical expertise - it demands a strong focus on risk management and governance. Regulators are paying close attention. For instance, in early 2025, Two Sigma Investments faced $90 million in penalties after employees made unauthorized changes to algorithmic trading parameters without proper approvals. Similarly, in August 2024, FINRA fined Brex Treasury $900,000 for using a flawed identity-verification algorithm, which led to poorly vetted accounts attempting over $15 million in transactions. These cases highlight the importance of having solid AI governance frameworks in place.

Model Risk Management and Explainability

The SEC and FINRA have made it clear: even when AI replaces manual processes, institutions must still meet their obligations for supervision, recordkeeping, and risk management.

In April 2026, the Federal Reserve, OCC, and FDIC issued SR letter 26-2, which distinguished between traditional AI models and newer generative or agentic AI. While traditional models remain under existing risk management guidelines, newer AI types require updated governance strategies.

"The revised guidance now applies narrowly to traditional models and basic AI applications. Going forward, we expect other risk-management and governance practices to support adoption of generative and agentic AI in ways that will encourage ongoing innovation." - Michelle W. Bowman, Vice Chair for Supervision, Federal Reserve Board

Explainability is another key requirement. When an AI system denies a loan or flags a transaction, regulators expect clear and defensible explanations. The Government Accountability Office (GAO) has warned:

"Insufficient explainability in AI models can... inhibit a financial institution's understanding of a model's conceptual soundness and reliability, inhibit independent review and audit, and make compliance with laws and regulations more difficult." - GAO-25-107197 Report

Explainable AI (XAI) tools are particularly useful in meeting adverse action notice requirements under the Equal Credit Opportunity Act and Fair Housing Act. Institutions can also enhance compliance by maintaining a detailed model inventory with assigned risk ratings and conducting independent model validations.

Identifying and Reducing Bias in AI Models

Beyond explainability, addressing bias in AI models is equally critical. AI systems trained on historical financial data may unintentionally replicate past discrimination. For example, using zip codes or social media activity as inputs can act as proxies for race or gender, even if those attributes aren't explicitly included - a phenomenon known as proxy bias.

Efforts to reduce bias can have measurable outcomes. One AI provider reported that credit unions using its model saw a 40% increase in credit approvals for women and people of color compared to traditional underwriting methods. However, achieving this requires ongoing monitoring, not just a one-time audit.

Regulators expect institutions to regularly test for disparate impacts and document their findings. For high-stakes applications like credit decisions, fairness checks across protected classes must be continuous. Effective governance also means involving cross-functional teams that include legal, compliance, risk, and business experts, alongside data scientists.

Data Privacy and Security

AI systems process vast amounts of data, which increases their vulnerability to cybersecurity threats. This makes robust security measures a critical part of risk management.

The evolving cyber threat landscape presents real dangers. In early 2024, an employee at a global financial institution was duped into transferring $25 million after participating in a video call featuring an AI-generated deepfake of the firm's CFO. By May 2026, U.S. Treasury and Federal Reserve officials were discussing the risks of Anthropic's Mythos model - a powerful AI capable of identifying cyber vulnerabilities - being exploited against banking systems.

"If an AI model acts on its own and is capable of updating its reasoning with no human intervention, this may undermine accountability for wrongdoing or errors." - Nellie Liang, Under Secretary for Domestic Finance, U.S. Treasury

To mitigate these risks, financial institutions should implement several practical measures:

Keep development and production environments strictly separate.

Encrypt sensitive customer data both at rest and in transit.

Incorporate AI-specific threat scenarios into existing cybersecurity programs.

Vendor risk management is another priority. Outsourcing AI functions to third-party providers doesn’t absolve institutions of compliance responsibilities. Conducting thorough due diligence on vendors, including gaining full visibility into their model operations and data flows, is essential.

A Roadmap for AI Adoption in Financial Institutions

Financial institutions are increasingly focused on scaling AI initiatives, but success requires more than just strong governance and data infrastructure. A clear execution plan is essential to turn AI ambitions into measurable business outcomes. While the financial sector boasts a 47% AI adoption rate and an average ROI of 180%, many projects - 68%, to be exact - fail to move beyond the pilot stage. The challenge isn’t a lack of ambition but rather the absence of structured execution.

Identifying High-Impact Use Cases

The first step is selecting use cases with care. Instead of jumping into complex applications, institutions should identify 40–80 potential AI use cases across areas like retail banking, corporate finance, wealth management, and insurance. Each use case should then be classified by regulatory risk, creating two deployment paths: a "fast-track" for low-risk, internal applications and a "governed-track" for high-risk, customer-facing models like credit scoring.

To prioritize effectively, evaluate use cases based on three factors: Business Impact (40%), Technical Feasibility (35%), and Implementation Speed (25%). Pay special attention to legacy system integration, as it’s a common stumbling block. High-risk models, such as AI-driven credit scoring, often require an additional 6–12 months and $220,000–$550,000 to meet compliance requirements.

Use Case

Risk Tier

Business Impact

Implementation Speed

Real-time Fraud Detection

Limited

9/10

8/10 (Fast)

KYC/AML Processing

Minimal

8/10

7/10 (Moderate)

AI Credit Scoring

High

9/10

4/10 (Slow)

Customer Service Bots

Limited

7/10

8/10 (Fast)

For most institutions, fraud detection and KYC automation are excellent starting points. These areas offer high returns, manageable data challenges, and minimal regulatory hurdles. For example, HSBC’s AI-powered KYC platform reduced customer onboarding time from five days to just four hours, while improving compliance accuracy by 25% in March 2026.

Once high-impact use cases are identified, institutions can move to a phased deployment approach.

Phased Rollout and Change Management

A phased rollout ensures a smooth transition from pilot to production. A typical roadmap includes three stages: Foundation (months 1–6), Controlled Deployment (months 6–18), and Scaling (months 18–36).

One critical step is shadow mode deployment. This involves running models on live data without making decisions, allowing teams to identify edge cases and build confidence among stakeholders. For instance, JPMorgan Chase used shadow mode to safely transition its AI-powered trading surveillance system to full production over 14 months in 2025, achieving zero regulatory issues.

DBS Bank provides another example of effective rollout. Between 2023 and 2025, the bank established an "AI factory" with a centralized team of over 800 data professionals and standardized processes. This reduced the average time to deploy a model from 12 months to just three, while boosting project success rates from 35% to 72%.

"The frontier of competition has moved from model development to model operations. The financial institutions winning with AI are those that have industrialized the entire lifecycle." - Vignesh Prajapati, Pingax Team

Change management is just as crucial as technical execution. Embedding AI champions within business units - such as compliance, credit, and operations - rather than treating AI as an IT project can triple the rate of successful production deployments.

Measuring ROI and Refining Your Approach

To assess AI’s impact, institutions must look beyond individual projects. With 45% of financial AI initiatives failing to reach production, it’s vital to evaluate ROI at the portfolio level, factoring in experimentation costs and overall returns.

A solid ROI framework includes four areas: direct financial returns (e.g., profit and loss impact), risk mitigation value (avoided losses or penalties), total cost of ownership (including compliance costs), and strategic value (competitive edge). Given that compliance and audit costs in financial services can be 20–500% higher than in less-regulated industries, these elements must be included in the business case.

For example, JPMorgan Chase’s COiN system automates contract reviews, saving 360,000 legal work hours annually and generating nearly $1.5 billion in cumulative cost savings. Similarly, Santander reported a 22% increase in product-per-customer ratios after deploying AI-driven next-best-action recommendations, resulting in $375 million in additional annual revenue across Europe. These successes highlight the importance of setting clear metrics before deployment and continuously refining them.

"The real value capture happens when institutions fine-tune these models on their proprietary transaction data, customer interaction histories and market intelligence, creating AI capabilities that competitors cannot replicate." - Helen Yu, CEO, Tigon Advisory Corp

Key metrics to track include fraud loss reductions, loan approval rates, KYC processing times, false positive rates in AML screening, and customer satisfaction scores. If a metric stagnates or declines, it’s a signal to retrain the model, adjust thresholds, or revisit the data - rather than giving up on the initiative.

The Future of AI in Financial Services

AI has firmly established itself as a cornerstone of financial services, moving far beyond the experimental phase. Today, 94% of financial services firms are actively piloting or implementing generative AI across key areas like pricing, risk management, and cybersecurity. The global AI-in-fintech market is also on track to hit $45 billion by 2026. This rapid adoption is reshaping how products are designed, delivered, and governed, setting the stage for the rise of agentic AI.

The next big leap is agentic AI. Unlike traditional systems that focus on predictions, agentic AI can autonomously plan and execute complex multi-step workflows. This capability addresses earlier challenges like manual feature engineering and disjointed pilot programs. For example, in June 2026, Revolut collaborated with NVIDIA to deploy PRAGMA, a transformer-based model trained on 24 billion events across 26 million user records. The result? PRAGMA outperformed task-specific models in credit scoring and fraud detection, eliminating weeks of manual work. Similarly, in 2025, Stripe's AI platform prevented $112 billion in fraud, reducing fraud rates by an average of 38% through its ability to analyze transactional behavior in context. These milestones are setting a new benchmark for the industry.

"AI in fintech is no longer an edge - it's the product." - Neomeric

As AI adoption accelerates, regulatory scrutiny is following close behind. Explainability has become a non-negotiable requirement. The 2026 SR 26-2 guidance issued by the Federal Reserve, OCC, and FDIC made it clear that traditional model risk management frameworks are inadequate for generative and agentic AI. Financial institutions must now develop governance structures tailored specifically for these advanced systems. Products that fail to provide clear, plain-language explanations for their decisions risk being rejected or pulled from the market. Meeting these demands requires a solid technical foundation.

Companies like Optiblack are stepping in to address these challenges with solutions like their AI Accelerator, Data Infrastructure, and Product Accelerator services. These tools are designed to help financial services firms transition from fragmented pilot projects to fully operational AI systems. By embedding governance, data lineage, and explainability from the start - rather than adding them as afterthoughts - these services ensure compliance while enabling innovation. As the industry continues to evolve, such foundational tools will be essential for building AI systems that are both effective and aligned with regulatory expectations.

FAQs

Where should a bank start with AI to get quick wins?

Banks can see immediate benefits from AI by prioritizing fraud detection systems and internal knowledge management. These areas strike a great balance between delivering high returns on investment and avoiding significant regulatory hurdles. This approach not only builds confidence among stakeholders but also ensures smooth adoption within existing workflows. By starting here, banks can create a reliable springboard for expanding AI into more intricate tasks, such as automated underwriting.

How can AI decisions be explained to regulators and customers?

Explaining how AI makes decisions is about finding the sweet spot between being transparent and meeting the audience’s needs. This is where Explainable AI (XAI) techniques come into play, offering justifications that humans can easily understand.

For customers, clear, actionable examples are key. Take counterfactuals, for instance: they show what could change to alter an outcome. Imagine telling a customer, "Your loan application would be approved if your income were $5,000 higher." Simple, direct, and actionable.

For regulators, the approach is a bit more technical. Tools like SHAP, LIME, or decision trees are invaluable for breaking down decisions in a way that satisfies compliance and scrutiny. These tools help dissect the "why" behind a model's output.

Ultimately, explanations should match both the complexity of the AI model and the significance of the decision being made. A straightforward decision might need a simpler explanation, while high-stakes scenarios demand more detailed insights.

What data foundation is needed before scaling AI in finance?

To effectively implement AI in financial services, organizations must establish a unified and well-managed data foundation. This means breaking down data silos and creating a single source of truth - often achieved through a lakehouse architecture that combines storage, computing power, and governance in one system.

Critical components of this approach include integrating data lineage, ensuring quality, and applying strict access controls directly within data pipelines. These measures enable real-time decision-making, consistent business definitions, and robust metadata management, all of which are essential for maintaining compliance and ensuring AI models remain transparent and explainable.

Explore how real-time AI-powered risk reporting enhances decision-making and risk management by providing continuous insights and predictive...

Vishal Rewari

Aug 5, 2025

Get notified on new marketing insights

Be the first to know about new B2B SaaS Marketing insights to build or refine your marketing function with the tools and knowledge of today’s industry.